Fix and Flip: The Complete Guide to House Flipping in 2026

House flipping can generate substantial profits — or wipe you out. This guide covers how to find deals, run the numbers with the 70% rule, finance a flip, budget the rehab, and avoid common mistakes.

Fix and flip — buying a distressed property, renovating it, and selling it for a profit — is one of the most visible strategies in real estate investing. TV shows make it look easy. The reality is more nuanced: successful flippers operate on thin margins where cost overruns and soft markets can quickly turn a profit into a loss.

This guide covers everything you need to know to evaluate a flip, fund it, execute the rehab, and sell profitably — including the numbers and mistakes that matter most.

How Fix and Flip Works

The basic model is straightforward:

- Find a distressed property priced below its potential market value.

- Finance the acquisition and rehab — typically with hard money or private money.

- Renovate to raise the property to market condition (or above).

- List and sell at the after-repair value (ARV).

- Profit = ARV minus all costs.

The challenge is in the execution: finding deals with enough spread, controlling rehab costs, managing carrying costs, and selling quickly in whatever market conditions exist at closing.

The 70% Rule

The 70% rule is the quick-filter every flipper uses to screen deals before running detailed numbers:

Maximum Allowable Offer (MAO) = ARV × 70% − Estimated Rehab Costs

The 30% buffer covers: profit, hard money interest, closing costs on both sides, holding costs (taxes, insurance, utilities), and any unexpected overruns.

Example:

- ARV: $280,000

- Estimated rehab: $45,000

- MAO = $280,000 × 70% − $45,000 = $196,000 − $45,000 = $151,000

If you can buy the property for $151,000 or less, the deal might work. The 70% rule is a screening tool, not a guarantee — always run the full numbers.

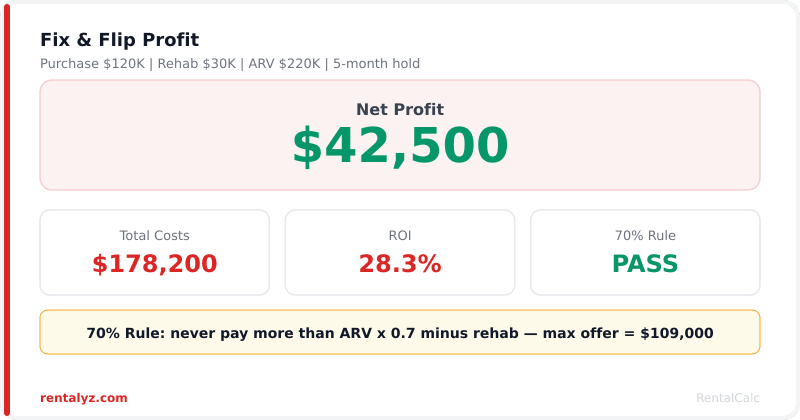

The Full Flip Math

A deal that passes the 70% rule still needs a complete financial model:

Acquisition costs:

- Purchase price: $148,000

- Closing costs (buy side): $3,200

- Hard money origination (2 points): $2,960

Rehab:

- Contracted rehab budget: $44,000

- Contingency (15%): $6,600

- Total rehab budget: $50,600

Carrying costs (6-month hold):

- Hard money interest (11% on $185,000): $10,175

- Property taxes (prorated): $1,400

- Insurance: $900

- Utilities: $600

- Total carrying: $13,075

Selling costs:

- Agent commissions (5%): $14,000 (on $280,000 ARV)

- Closing costs (sell side): $3,500

- Staging: $2,500

- Total selling: $20,000

Total cost basis: $148,000 + $3,200 + $2,960 + $50,600 + $13,075 + $20,000 = $237,835

Gross profit: $280,000 − $237,835 = $42,165

Return on investment: $42,165 ÷ $52,460 total cash invested = 80% ROI (annualized over 6 months ≈ 160% annualized — but remember, this involves significant risk and active management)

Finding Deals

Deals don’t come to you on the MLS at discount prices. You have to build a pipeline:

Driving for dollars: Identify properties that show signs of neglect (overgrown lawn, boarded windows, deferred maintenance) and trace the owner through county records or skip-tracing services.

Direct mail: Send postcards or letters to absentee owners, out-of-state owners, pre-foreclosure lists, and probate estates. Expect 0.5%–2% response rates — it’s a volume game.

Wholesalers: Investors who specialize in finding and contracting distressed properties, then assigning those contracts for a fee. Buying from a wholesaler saves your marketing time but adds a $5,000–$20,000 assignment fee to your cost basis.

Foreclosure auctions: County courthouse steps or online auction platforms (Auction.com, Hubzu). You bid without seeing the interior, often without a title search. High risk, high potential reward. For experienced investors only.

Probate and estate attorneys: Heirs often want to liquidate quickly. Building relationships with local probate attorneys can provide a steady deal flow.

Bank REOs (Real Estate Owned): Banks that have foreclosed on properties and now own them. Listed on the MLS and through asset managers. Less discount than pre-foreclosure but more conventional transaction process.

Expect to look at 20–50 leads to find one deal worth pursuing. Volume in, deals out.

Financing a Flip

Most residential lenders won’t finance a property that needs significant work. Your options:

Hard Money Loans

The most common flip financing. Terms vary, but expect:

- Rates: 10%–14% annually

- Points: 1–3 points at origination (1 point = 1% of loan amount)

- LTV: Typically 65%–75% of ARV, or 80%–90% of purchase price

- Rehab draws: Lender releases rehab funds in tranches as work is completed and inspected

- Term: 6–18 months

- Speed: Can close in 5–15 days — critical for competitive auction deals

Hard money is expensive but purpose-built for flips. Run the carrying cost before you commit.

Private Money

Loans from private individuals (friends, family, other investors) at negotiated terms. Usually cheaper than hard money, more flexible, but requires a network and track record.

Cash

Cleanest option. No carrying cost on the loan, fastest close, full control of rehab timeline. Requires significant liquid capital.

Home Equity (HELOC or Cash-Out Refi)

If you own a primary residence with equity, you can borrow against it to fund the flip. Lower rate than hard money, but ties your home to the deal’s outcome.

Budgeting the Rehab

Rehab cost overruns are the most common way flips go wrong. Here’s how to get to accurate numbers:

Get 3 contractor bids. Never use the first number you’re given. Require itemized bids (not “gut the kitchen for $22,000” but line-item costs for demo, cabinets, countertops, appliances, labor).

Don’t over-improve. Match the finish level to the neighborhood. Granite countertops in a $180,000 ARV market won’t return their cost. Laminate that looks good photographed? Fine.

Budget by scope category:

| Scope | Typical Range (1,400 sq ft SFR) |

|---|---|

| Kitchen remodel (mid-range) | $12,000–$25,000 |

| Bathroom remodel (per bath) | $6,000–$15,000 |

| Flooring (LVP, whole house) | $8,000–$16,000 |

| Paint (interior, whole house) | $3,000–$6,000 |

| Roof replacement | $8,000–$18,000 |

| HVAC replacement | $6,000–$12,000 |

| Electrical update | $4,000–$12,000 |

| Plumbing update | $3,000–$10,000 |

| Landscaping / curb appeal | $2,000–$8,000 |

Always build in a contingency. Budget 15% over your estimated costs. If you don’t use it, that’s profit. If you need it, you won’t be surprised.

Selling the Flip

The exit is as important as the buy. Mistakes here eat into profit:

Price correctly from day one. Overpriced flips sit on the market, accumulate carrying costs, and often require price reductions that wipe out the pricing premium you were hoping for. Study the comps honestly.

Photograph professionally. A $500 photography session routinely results in faster sales and higher offers. It’s one of the highest-ROI line items in the flip.

Stage at least minimally. Empty houses feel smaller and sell slower. Even minimal furniture staging helps buyers envision the space.

Understand your holding cost per day. If you’re carrying $200,000 in hard money at 12%, that’s $24,000/year or $66/day. A 30-day price reduction delay costs $2,000 in carrying — which might be less than a significant price cut. Price it right and get out cleanly.

Common Fix and Flip Mistakes

Overestimating ARV. Use comparable sales from the last 90 days within 0.5 miles and similar square footage. Don’t cherry-pick the highest sale and assume you’ll match it.

Underestimating rehab. Get professional bids. Inspect the roof, HVAC, plumbing, and electrical before you make an offer. Surprises in these systems are expensive.

Ignoring the exit market. Flipping in a declining market means your ARV when you sell might be less than your ARV when you bought. Timing matters.

Hiring the cheapest contractor. Low bids often reflect incomplete scope, unskilled labor, or a contractor who will disappear mid-project. Check references, pull permits, require insurance.

Not pulling permits. Unpermitted work (especially electrical and structural) can surface in the buyer’s inspection and kill the deal. Pull permits and do it right.

Running out of capital. Always have a reserve. If the rehab runs over and you can’t fund the overrun, the project stalls — and a stalled flip is an expensive one.

Fix and Flip vs. Buy and Hold

The fundamental choice in real estate investing:

| Factor | Fix and Flip | Buy and Hold |

|---|---|---|

| Time horizon | 6–18 months | Years to decades |

| Income type | Lump sum profit (taxed as ordinary income if under 1 year) | Recurring cash flow + appreciation |

| Capital recycling | Yes — redeploy after each deal | No — capital stays in the asset |

| Financing | Hard money / private money | Conventional / DSCR / portfolio |

| Active involvement | High | Lower (especially with PM) |

| Market timing risk | High | Lower |

| Tax efficiency | Lower (short-term capital gains) | Higher (depreciation, long-term gains, 1031 exchanges) |

Many investors start with flips to build capital, then transition to buy-and-hold for passive income and tax efficiency.

Frequently Asked Questions

Q: What is the 70% rule in house flipping?

Maximum offer = ARV × 70% minus estimated rehab. On a $300,000 ARV property with a $50,000 rehab, that’s $160,000 max offer. The 30% buffer covers profit, financing, and selling costs.

Q: How much money do you need to start flipping?

With hard money, expect 10%–25% down plus reserves. In a mid-priced market, $40,000–$100,000 in liquid capital is a reasonable starting point for a first flip.

Q: How long does a house flip take?

Typically 3–9 months from purchase to sale. Rehab scope and contractor efficiency drive most of the variance.

Q: Is fix and flip taxed as ordinary income?

Profits from flips held under 12 months are taxed as short-term capital gains — same rate as ordinary income. Frequent flippers may also face self-employment taxes.

Run the Numbers on Your Flip

Use our free flip calculator to model ARV, rehab costs, carrying costs, and projected profit — no signup required.