The BRRRR Method: Complete Guide to Buy, Rehab, Rent, Refinance, Repeat

The BRRRR method lets you recycle your down payment across multiple rental properties. This guide walks through every step with real numbers, financing options, and what can go wrong.

The BRRRR method is how many investors build a rental portfolio without needing a new pile of cash for every deal. The acronym stands for Buy, Rehab, Rent, Refinance, Repeat — and the core idea is that you buy a distressed property cheaply, force appreciation through renovation, rent it out to qualify for a loan, then pull your original capital back out through a cash-out refinance. Then you do it again.

Done well, BRRRR can dramatically accelerate portfolio growth. Done poorly, it traps your cash and leaves you with a problem property you can’t escape. This guide walks through every step with real numbers so you can evaluate whether it makes sense for you.

How BRRRR Works: The Full Cycle

Step 1: Buy

You’re not looking for a turnkey property. You’re looking for a distressed property priced below its after-repair value (ARV). Distressed means: deferred maintenance, cosmetic neglect, an estate sale, a motivated seller, or some combination. The discount is where your profit (and your refinanced capital) comes from.

The target: Purchase price + rehab costs should total no more than 70%–75% of ARV.

Example property:

- ARV (after-repair value): $200,000

- 70% of ARV: $140,000

- Target: purchase price + rehab ≤ $140,000

Step 2: Rehab

The rehab must be focused on value and rentability — not personal taste. Kitchens, bathrooms, flooring, and paint move the needle. Swimming pools and custom finishes rarely produce a dollar-for-dollar return.

Rehab budget rule of thumb: Plan for overruns. Budget for what you expect, add 15%–20%, and keep a contingency reserve on top of that.

Continuing the example:

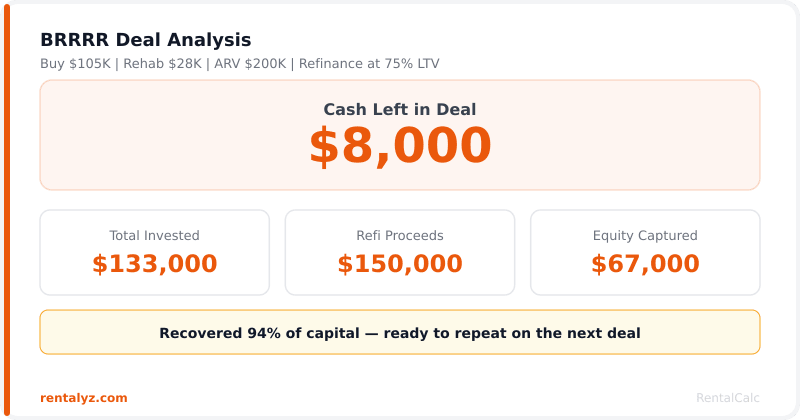

- Purchase price: $105,000

- Rehab cost: $28,000

- Total invested: $133,000 (67% of ARV — within target)

A common mistake is letting the rehab scope creep until the numbers stop working. Every dollar of scope creep either comes out of your margin or traps more capital in the deal.

Step 3: Rent

Before you can refinance, you need the property rented and ideally seasoned (meaning the tenant has been in place for a period of time — often 6 months, though this varies by lender). The rental income is what justifies the loan.

Key metrics lenders look at:

- DSCR (Debt Service Coverage Ratio): Net operating income ÷ annual debt service. Most DSCR lenders want 1.20 or higher.

- Market rent confirmed by an appraisal.

Continuing the example:

- Monthly rent: $1,600

- Annual rent: $19,200

- Operating expenses: $7,200/year (taxes, insurance, management, maintenance)

- NOI: $12,000

- ARV: $200,000 — confirmed by appraisal

Step 4: Refinance

This is the engine of the strategy. You do a cash-out refinance at the property’s new, higher appraised value — not what you paid for it.

Refinance math:

- Appraised value: $200,000

- Lender LTV limit (75%): $150,000 maximum loan

- Cash-out proceeds: $150,000

Your cash in: $133,000 Cash back: $150,000 Net cash recovered: $17,000 more than you put in

In this ideal scenario, you not only got your money back — you walked away with extra cash and a rental property with built-in equity. In practice, most deals land somewhere between recovering 80%–100% of invested capital.

Step 5: Repeat

Take the recovered cash and find the next deal. Each cycle builds your portfolio without requiring fresh savings for every property.

Finding BRRRR Deals

Distressed properties don’t show up on Zillow at below-market prices. You have to go find them.

Where to look:

- Driving for dollars — physically driving neighborhoods and noting vacant, overgrown, or boarded properties, then skip-tracing the owner.

- Direct mail — sending letters or postcards to absentee owners, probate estates, and tax-delinquent properties.

- Wholesalers — investors who contract properties and sell their position to other buyers. You pay a wholesale fee, but skip the marketing work.

- MLS listings with long days on market — properties that have been sitting often have motivated sellers.

- Foreclosure auctions — high potential discount, but you usually buy sight-unseen and take on title risk. Research carefully.

- Estate sales and probate — heirs often want to liquidate quickly.

Expect to analyze 20–30 leads to get to one deal that works.

Financing the Purchase and Rehab

You cannot use a 30-year conventional mortgage to buy a property that needs significant work — Fannie/Freddie won’t lend on it. Your financing options at acquisition:

Hard money loans: Short-term (6–18 months), asset-based lending. Rates typically run 10%–14% plus points. Fast to close, lends on ARV not purchase price, but expensive. Best for experienced investors who can execute quickly.

Private money: Friends, family, or private investors who lend at negotiated terms. Often cheaper than hard money and more flexible. Requires a network and track record.

Portfolio lenders / local banks: Community banks that keep loans on their own books (instead of selling to Fannie Mae) can lend on distressed properties. Rates are in between conventional and hard money. Worth calling local banks and credit unions.

HELOC or cash-out refi on existing property: If you already own a home with equity, you can tap it to fund the purchase and rehab. Lowest cost of funds, but ties risk to your primary residence.

Cash: Cleanest option — no lender conditions, fastest close, no carrying cost on the loan. Requires having the capital available.

The Cash-Out Refinance

After rehab and lease-up, you refinance into a permanent loan — usually a 30-year DSCR loan or a conventional investment property loan.

Key refinance considerations:

- Seasoning requirements: Many lenders require 6–12 months of ownership before a cash-out refinance. Some DSCR lenders will do a “delayed financing” refinance immediately if you purchased all-cash. Clarify this with your lender before you buy.

- Appraisal: The refinance is only as good as the appraised value. Make sure the ARV estimate before you buy is backed by real comparable sales (comps), not wishful thinking.

- LTV limits: Most lenders cap investment property cash-out refinances at 70%–75% LTV. At 75% LTV, a $200,000 appraisal yields a maximum $150,000 loan.

- DSCR minimums: DSCR lenders will calculate whether the rent supports the new loan payment. Run the numbers before you commit.

Real Numbers: A Full BRRRR Cycle

Here is a complete example showing all the math in one place.

Acquisition phase:

- Purchase price: $105,000 (hard money, 12% rate, 2 points)

- Rehab: $28,000

- Closing costs (acquisition): $2,500

- Carrying costs (6 months hard money): $7,560

- Total cash invested: $143,060

After rehab:

- Appraised value: $205,000

- Monthly rent: $1,650

Refinance:

- Loan at 75% LTV: $153,750

- Closing costs (refinance): $4,200

- Net cash out: $153,750 − $4,200 = $149,550

Results:

- Cash recovered: $149,550 of $143,060 invested = 104.5% returned

- Cash left in deal: $0 (actually +$6,490 in pocket)

- Monthly cash flow: $1,650 rent − $950 PITI − $550 operating expenses = $150/month

- Equity at purchase: $205,000 − $153,750 = $51,250

The cash flow is modest, but the equity position is real and the capital is free to deploy again.

Risks and What Can Go Wrong

Rehab cost overruns: The single most common failure mode. A $28,000 budget that becomes $42,000 can collapse the deal math entirely.

Appraisal comes in low: If the appraisal doesn’t support the expected ARV, your cash-out loan will be smaller and you’ll leave more capital trapped in the deal.

Rental market softness: If rents are lower than you projected, the DSCR might not meet the lender’s minimums.

Carrying costs accumulate: Every extra month you spend on rehab is another month of hard money interest. A six-month project that takes nine months costs significantly more.

Lender seasoning requirements change: Lending standards evolve. What your lender told you at acquisition might change by the time you’re ready to refinance. Get everything in writing and confirm requirements with multiple lenders.

Forced appreciation reverses: In a declining market, properties may not appraise at the expected ARV even after rehab. BRRRR works best in stable or appreciating markets.

When BRRRR Doesn’t Work

BRRRR is not a fit for every investor or every market.

- High-cost markets — In markets where ARV is $800,000+ and rental yields are thin, the numbers rarely work. The rent doesn’t support the DSCR on a 75% LTV refinance.

- Investors without a rehab team — Without reliable contractors at reasonable prices, rehab costs will eat your margin.

- First-time investors without reserves — BRRRR deals frequently need emergency funds. Going in without 6 months of reserves is a common mistake.

- Markets with long lease-up periods — If vacancy runs 3–6 months in your market, the carrying costs during lease-up kill the deal.

Frequently Asked Questions

Q: How much money do I need to start BRRRR?

Enough to cover the purchase, rehab, carrying costs, closing costs, and reserves. In a mid-priced market, expect $50,000–$150,000 in liquid capital for the first deal — most of which you’ll get back through the refinance.

Q: What is the 70% rule in BRRRR?

Total investment (purchase + rehab) should not exceed 70% of ARV. This ensures enough equity to support the refinance and leaves room for overruns.

Q: Can you BRRRR with no money down?

Theoretically yes if the refinance returns 100%+ of capital (called an “infinite return”). In practice, 80%–105% capital recovery is more realistic.

Q: How long does a BRRRR cycle take?

Typically 9–18 months total: deal-finding (1–3 months), rehab (2–6 months), lease-up (1–2 months), and refinance including seasoning requirements.

Run the Numbers on Your BRRRR Deal

Use our free BRRRR calculator to model your deal — purchase price, rehab, ARV, refinance, and projected returns.