DSCR Loans: Requirements, Rates & How to Qualify in 2026

DSCR loans let real estate investors qualify based on rental income — not personal income or W-2s. Learn the requirements, current rates, and how to structure your deal to qualify.

DSCR loans have become one of the most popular financing tools for real estate investors, and for good reason: you can qualify based entirely on the rental income the property generates, not your personal salary, tax returns, or W-2s. If you’re self-employed, have complex income, or already own several rental properties that complicate your debt-to-income ratio, a DSCR loan may be the cleanest path to your next acquisition.

This guide explains how DSCR loans work, exactly what lenders look for, current rate expectations, and how to structure your deal to qualify.

What Is a DSCR Loan?

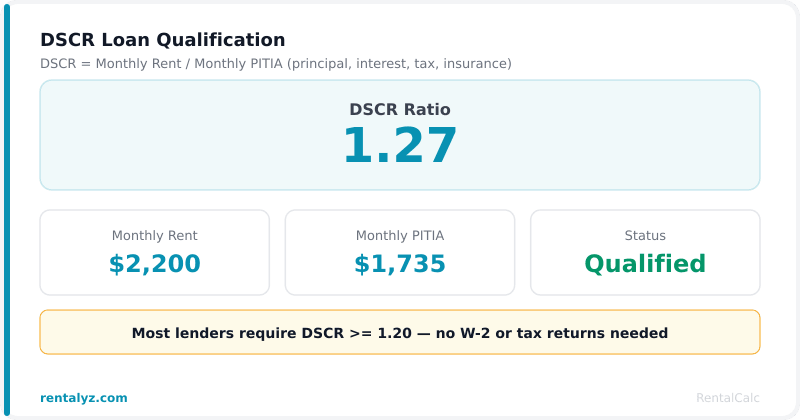

DSCR stands for Debt Service Coverage Ratio. It measures whether a property’s rental income is sufficient to cover its loan payments.

DSCR = Annual Net Operating Income ÷ Annual Debt Service

Or more precisely, many DSCR lenders use:

DSCR = Monthly Gross Rent ÷ Monthly PITIA

Where PITIA = Principal + Interest + Taxes + Insurance + HOA (if applicable).

Example:

- Monthly rent: $2,200

- Monthly PITIA: $1,750

- DSCR: $2,200 ÷ $1,750 = 1.26

A DSCR above 1.0 means the property generates more income than it costs to carry. A DSCR below 1.0 means the rent doesn’t fully cover the mortgage payment.

Most DSCR lenders require a minimum ratio of 1.20–1.25, though some offer “no-ratio” or “DSCR below 1.0” products at higher rates and stricter LTV limits.

Who DSCR Loans Are For

DSCR loans were designed specifically for real estate investors. They are a strong fit if you:

- Are self-employed or have irregular/1099 income that makes traditional qualification difficult

- Own multiple rental properties and your conventional debt-to-income ratio is already stretched

- Want to scale your portfolio faster without waiting for W-2 income growth

- Are buying in an LLC or other entity structure (many DSCR lenders allow this; conventional Fannie/Freddie loans typically do not)

- Are a foreign national or recent immigrant without extensive US credit history (some DSCR lenders accommodate this)

DSCR loans are not for primary residences or owner-occupied properties. They are investment property loans, period.

DSCR Loan Requirements in 2026

Requirements vary by lender, but here are the typical standards across the market:

Credit Score

Most DSCR lenders require a minimum 640–680 FICO score. Better rates and higher LTV are available at 720+. Some lenders go down to 620 with compensating factors (larger down payment, strong DSCR, reserves).

Down Payment / LTV

- Purchase: Most lenders cap LTV at 75%–80%, meaning a minimum 20%–25% down payment.

- Cash-out refinance: Typically 70%–75% LTV maximum.

- Rate-and-term refinance: Up to 80% LTV in some cases.

DSCR Ratio

- Standard: 1.20–1.25 minimum

- Preferred: 1.25+ for the best pricing

- Below 1.0 products: Available from some lenders at 65%–70% LTV with rate premiums of 0.5%–1.5%

- No-ratio products: Some lenders skip the DSCR calculation entirely for strong borrowers with significant reserves

Property Types

Most DSCR lenders finance:

- Single-family rentals (1–4 units)

- Condos (warrantable and some non-warrantable)

- Short-term rentals / Airbnb (using market-rate or STR income)

- 5–8 unit multifamily (at some lenders)

- Mixed-use with majority residential income (at some lenders)

Rural properties, mobile homes, and raw land are generally excluded.

Reserves

Lenders typically want to see 3–6 months of PITIA in reserves after closing. Some require more for short-term rentals or if the property is new construction.

Entity / LLC Borrowing

This is a major advantage of DSCR loans over conventional financing. Most DSCR lenders will lend directly to an LLC, LP, or corporation — keeping the property out of your personal name for liability protection. Conventional Fannie/Freddie loans require personal guarantee and generally don’t allow LLC vesting.

Property Condition

The property must be in rentable condition. Unlike fix-and-flip hard money loans, DSCR lenders won’t lend on a gutted property mid-renovation. The appraisal needs to confirm the property is habitable and income-producing.

DSCR vs. Conventional Investment Property Loans

| Feature | DSCR Loan | Conventional (Fannie/Freddie) |

|---|---|---|

| Qualification basis | Property income | Personal income (DTI) |

| W-2 / tax returns required | No | Yes |

| LLC vesting | Allowed | Not allowed |

| Max financed properties | Unlimited (varies by lender) | 10 (Fannie Mae limit) |

| Self-employed friendly | Yes | Challenging |

| Rate premium vs. conventional | +0.5%–1.5% | Baseline |

| Loan limits | Often higher than conforming | Conforming limits apply |

| Cash-out refinance flexibility | Flexible | More restrictions |

The main trade-off is rate. DSCR loans typically run 0.5%–1.5% higher than conventional investment property loans with the same LTV. For investors who don’t qualify conventionally or who are beyond the 10-property limit, that premium is irrelevant — it’s the only option.

Current DSCR Loan Rates (2026)

DSCR loan rates change with the broader rate environment. As of early 2026, here are typical rate ranges:

| LTV | DSCR | Credit Score | Approximate Rate |

|---|---|---|---|

| 65% | 1.35+ | 740+ | 7.00%–7.50% |

| 70% | 1.25+ | 720+ | 7.25%–7.75% |

| 75% | 1.20+ | 700+ | 7.50%–8.00% |

| 75% | 1.10–1.20 | 680+ | 8.00%–8.75% |

| 70% | Below 1.0 | 700+ | 8.75%–9.50% |

These are 30-year fixed-rate products. Adjustable-rate DSCR products (5/1 ARM, 7/1 ARM) are available at lower initial rates.

Note: Rates include add-ons for short-term rental properties (typically +0.25%–0.75%) and for LLC/entity borrowing at some lenders (typically +0.125%–0.25%).

How to Calculate Your Property’s DSCR Before Applying

Run this math before you apply:

- Determine monthly rent: Use current lease rate. If vacant, the lender will order an appraisal with a rent schedule.

- Estimate PITIA: Principal + Interest (calculate at your expected rate and loan amount) + property taxes (annual ÷ 12) + insurance (annual ÷ 12) + HOA (if applicable).

- Divide rent by PITIA: The result is your DSCR.

Example:

- Monthly rent: $2,400

- Expected loan: $275,000 at 7.75% / 30 years → $1,969/month P&I

- Property taxes: $4,200/year → $350/month

- Insurance: $1,800/year → $150/month

- PITIA: $1,969 + $350 + $150 = $2,469/month

- DSCR: $2,400 ÷ $2,469 = 0.97

This deal doesn’t qualify at the standard 1.20 DSCR threshold. Your options: increase the rent, reduce the purchase price, or seek a no-ratio or below-1.0 DSCR product at higher rates and lower LTV.

Improving Your DSCR Before Applying

If your DSCR is too low, here’s how to fix it:

Put more money down. A larger down payment means a smaller loan and lower monthly P&I, which directly improves DSCR.

Find a property with higher rent. DSCR is a property-level calculation. Better income = better ratio.

Improve the property before applying. A short-term rental with documented higher income might qualify at a higher rent figure.

Negotiate a lower purchase price. Lower price = smaller loan = lower debt service = higher DSCR.

Compare lenders. DSCR calculation methods vary. Some use gross rent; others use net rent or an NOI approach. Different methods produce different ratios for the same property.

Short-Term Rental (STR) DSCR Loans

Using Airbnb income to qualify for a DSCR loan is possible, but lenders approach it differently:

- AirDNA or STR market data: Many lenders use third-party rental market data services to estimate STR income rather than actual Airbnb bookings. The lender will pull what similar properties in the area earn, then apply their own haircut (usually 60%–80% of the market estimate).

- Existing STR income: If the property has 12+ months of STR history with tax returns to back it up, some lenders will use actual trailing income.

- Standard long-term rent: Some lenders ignore the STR income and underwrite to the long-term market rent. This is more conservative but avoids STR-specific rate premiums.

The Application Process

- Get pre-qualified. Most DSCR lenders can give you a soft pre-qualification with just the property address, your credit score, expected loan amount, and projected rent. No income documentation required.

- Property goes under contract. Apply formally and lock your rate.

- Appraisal. The lender orders an appraisal that confirms value AND market rent (via a rent schedule). This is the critical document.

- Title search and insurance ordered.

- Entity documents (if applicable). Provide LLC operating agreement, articles of organization, etc.

- Clear to close. Most DSCR loans close in 21–30 days.

Frequently Asked Questions

Q: Can I get a DSCR loan with no income verification?

Yes. DSCR loans require no W-2s, tax returns, or personal income documentation. Qualification is based entirely on the property’s rental income vs. debt service.

Q: What is the minimum DSCR to qualify?

Most lenders require 1.20–1.25 minimum. Below-1.0 products exist at higher rates and lower LTV limits.

Q: Can I use a DSCR loan for an Airbnb property?

Yes. Most DSCR lenders accept STR properties, using third-party rental market data to estimate income. Expect a small rate premium (0.25%–0.75%) over standard rental property rates.

Q: How many DSCR loans can I have at once?

Unlike Fannie Mae (capped at 10 properties), DSCR lenders often have no universal cap. Many allow 10–20+ per borrower.

Calculate DSCR for Your Property

Use our free DSCR calculator to see whether your rental property meets lender thresholds before you apply.